Words of Expert Advice

Essential Money Management Tips

SEO Optimized Content

Personal Finance Tips for Everyone: A Global Guide to Financial Success

Managing personal finances effectively is one of the most important skills you can develop in today's economy. Whether you're just starting your financial journey or looking to optimize your existing strategy, understanding fundamental money management principles can transform your financial future. In this comprehensive guide, we'll explore essential personal finance tips that help people worldwide build wealth, reduce debt, and achieve their financial goals.

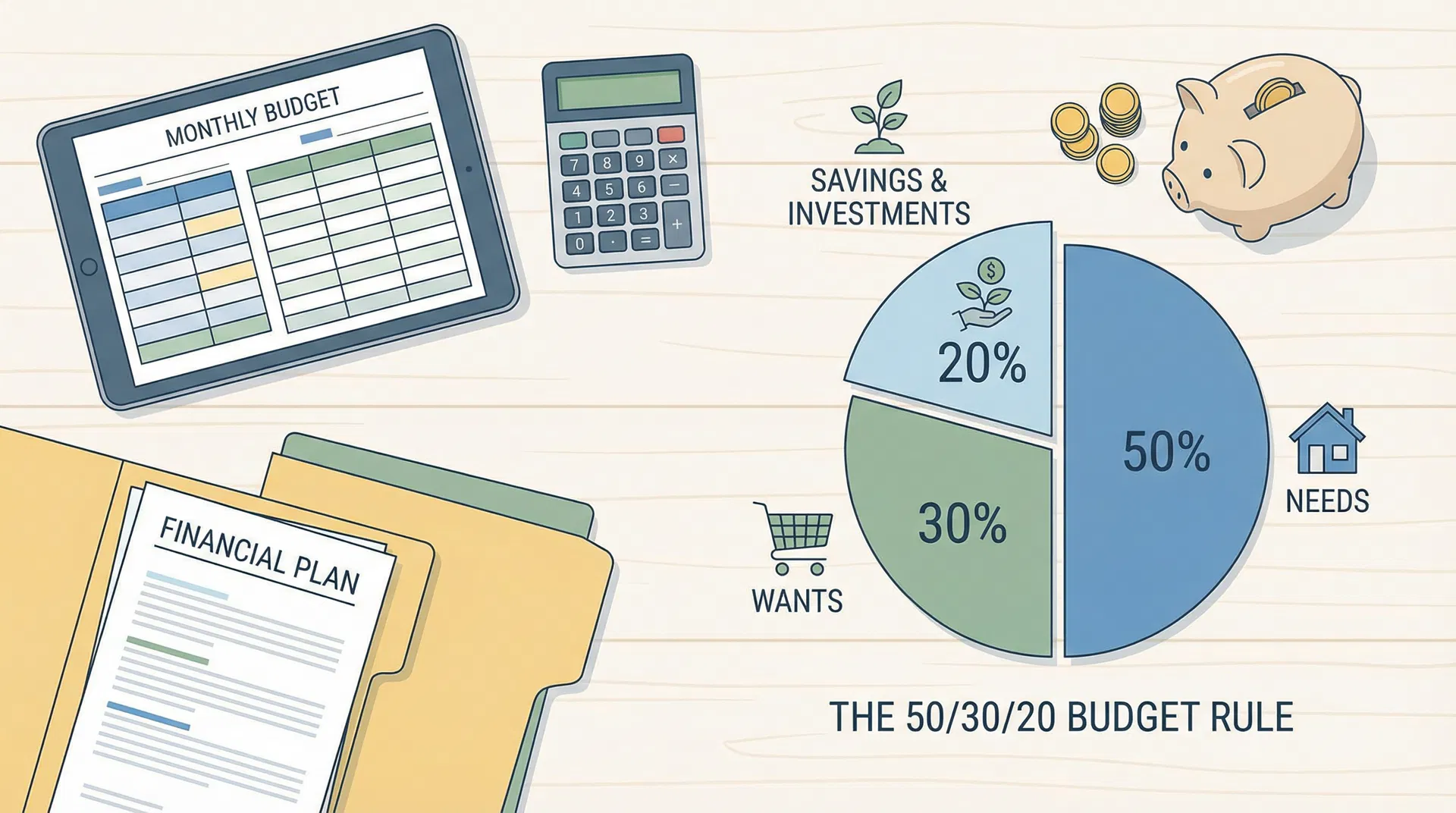

1. Create a Comprehensive Budget: The Foundation of Financial Success

A budget is the cornerstone of effective personal finance management. Creating and maintaining a budget helps you understand where your money goes each month and ensures you're spending within your means. Without a budget, you might run out of money before your next paycheck, leaving you vulnerable to financial stress and debt accumulation.

To create an effective budget, start by calculating your total monthly income from all sources. Next, list all your expenses, including fixed costs like rent or mortgage, utilities, insurance, and variable expenses like groceries, entertainment, and dining out. The 50/30/20 budgeting rule is a popular framework that many financial experts recommend, allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment.

2. Build an Emergency Fund: Your Financial Safety Net

An emergency fund is money set aside specifically for unexpected expenses or income loss. This financial cushion protects you from going into debt when emergencies arise, such as medical bills, car repairs, or job loss. Financial experts recommend maintaining an emergency fund equivalent to three to six months of living expenses.

Start by opening a separate savings account dedicated solely to your emergency fund. Begin by saving whatever amount you can afford each month, even if it's just $25 or $50. Consistency matters more than the amount at this stage. Once you've built your initial emergency fund of $1,000 to $2,000, focus on expanding it to cover three to six months of expenses.

3. Pay Off Debt Strategically: Eliminate Financial Burden

Debt is one of the biggest obstacles to financial freedom. High-interest debt, particularly credit card debt, can quickly spiral out of control if not managed properly. There are two popular debt repayment strategies: the debt snowball method and the debt avalanche method.

- Snowball Method: Pay off smallest debts first for quick wins

- Avalanche Method: Pay off highest interest rates first to save money

4. Automate Your Bill Payments: Ensure Consistency and Avoid Late Fees

Automating your bill payments is one of the simplest yet most effective personal finance strategies. Setting up automatic payments ensures you never miss a due date, which protects your credit score and saves you money on late fees. Late payments can damage your credit rating for up to seven years, making it harder to obtain loans and credit in the future.

Most banks and service providers offer automatic payment options. You can set up recurring payments for fixed bills like mortgage, rent, utilities, and insurance. This approach removes the mental burden of remembering multiple due dates and ensures consistent payment history.

5. Monitor and Improve Your Credit Score: Build Financial Credibility

Your credit score is a three-digit number that represents your creditworthiness. A higher credit score translates to better interest rates on loans, lower insurance premiums, and improved chances of loan approval. Focus on these key factors:

- • Payment History (35%): Pay all bills on time

- • Credit Utilization (30%): Keep balances below 30% of limits

- • Length of Credit History (15%): Maintain older accounts

- • Credit Mix (10%): Maintain diverse credit types

- • New Credit Inquiries (10%): Limit new applications

6. Maximize Your High-Yield Savings Account: Earn More on Your Money

Traditional savings accounts offer minimal interest rates, often less than 0.01% annually. High-yield savings accounts (HYSA) provide significantly better returns, currently offering 4% to 5% annual percentage yield (APY). By moving your emergency fund and short-term savings to a high-yield account, you can earn hundreds or thousands of dollars in additional interest annually.

High-yield savings accounts are FDIC-insured up to $250,000, making them a safe place to store your money while earning competitive returns. This combination of safety and returns makes them ideal for emergency funds and savings goals with shorter timeframes.

7. Plan for Retirement: Secure Your Financial Future

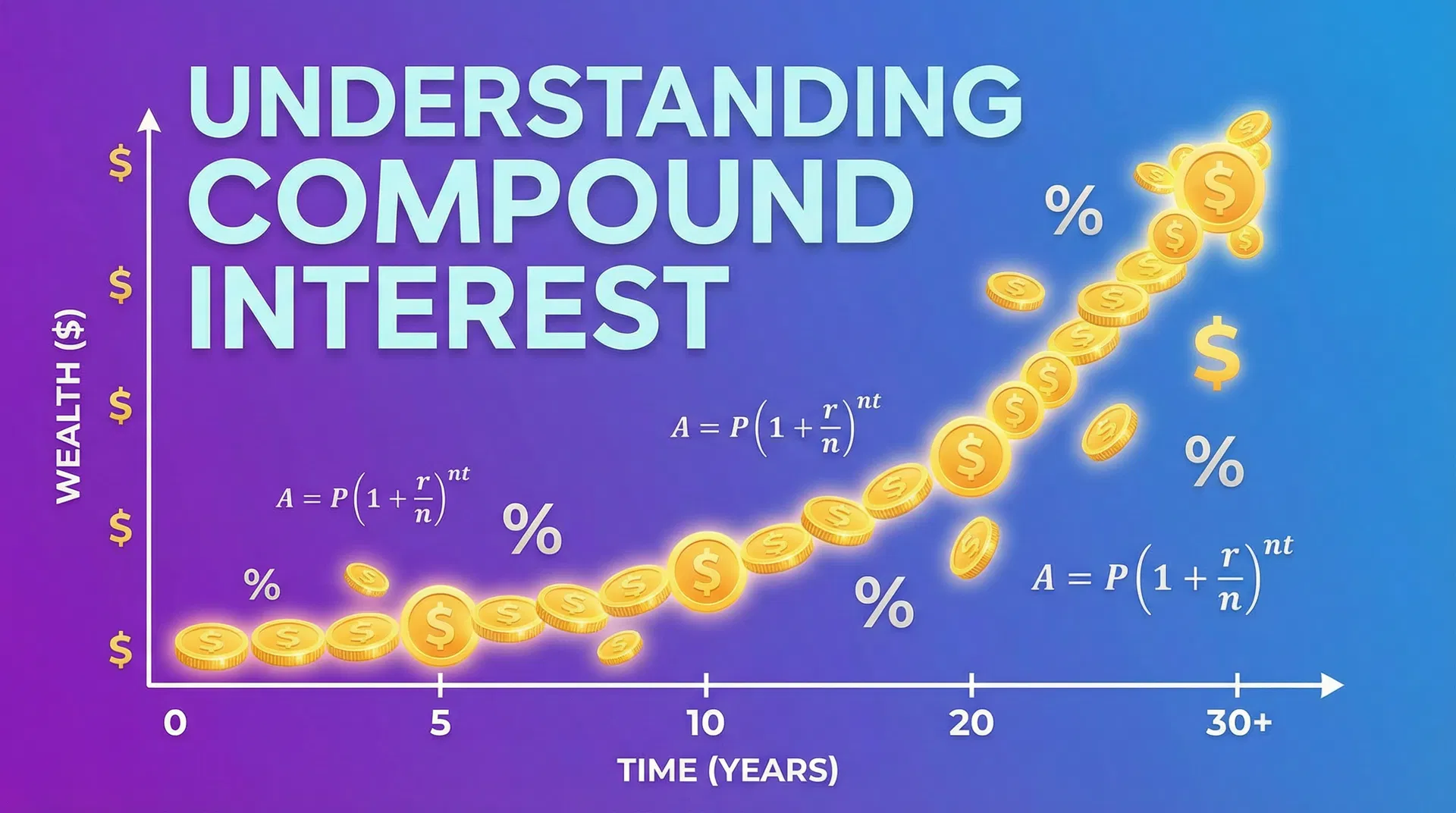

Retirement planning is a critical component of personal finance that many people neglect. Starting early allows you to take advantage of compound interest, which significantly increases your retirement savings over decades. If your employer offers a 401(k) plan, contribute enough to receive the full employer match—this is essentially free money.

If your employer doesn't offer a 401(k), consider opening an Individual Retirement Account (IRA). Traditional IRAs offer tax-deductible contributions, while Roth IRAs provide tax-free withdrawals in retirement. Many financial advisors suggest aiming to replace 70-80% of your pre-retirement income.

8. Set Clear Financial Goals: Create Your Roadmap to Success

Setting specific, measurable financial goals provides direction and motivation for your money management efforts. Rather than vague aspirations, establish concrete goals such as "save $10,000 for a down payment within 24 months" or "pay off $15,000 in credit card debt within 18 months."

Categorize your goals into short-term (less than one year), medium-term (one to five years), and long-term (more than five years). Write down your goals and review them regularly. Track your progress toward each goal and celebrate milestones along the way.

9. Track Your Spending: Understand Your Financial Habits

Tracking your spending reveals patterns and habits that might otherwise remain invisible. Many people are surprised to discover how much they spend on subscriptions, dining out, or impulse purchases. Use budgeting apps, spreadsheets, or even a simple notebook to record your daily spending.

Review your spending data monthly to identify trends. Look for subscriptions you've forgotten about, recurring charges you no longer need, and discretionary spending that could be reduced. This awareness is the first step toward making meaningful changes.

10. Invest in Your Future: Build Long-Term Wealth

While saving is important, investing is essential for building substantial long-term wealth. Inflation erodes the purchasing power of money saved in traditional accounts, making investment growth necessary to maintain and increase your wealth over time.

Start investing early, even with small amounts. Index funds and exchange-traded funds (ETFs) provide diversified investment exposure with minimal fees. These passive investment vehicles are ideal for beginners and offer consistent long-term growth. Consider your risk tolerance and investment timeline when choosing investments.

Conclusion: Take Action Today

Personal finance success doesn't happen overnight, but with consistent effort and smart decision-making, you can dramatically improve your financial situation. Start by implementing one or two strategies from this guide, then gradually add more as you build confidence and momentum.

Remember that personal finance is personal. What works for others might not work for you, and that's okay. The key is finding strategies that align with your values, goals, and lifestyle. Take action today by creating a budget, starting an emergency fund, or automating your bill payments. Your future self will thank you for the financial decisions you make now.

Start Building Your Emergency Fund Today

An emergency fund is your first line of defense against financial hardship. Whether it's a medical emergency, job loss, or unexpected home repair, having money set aside provides peace of mind and protects your financial stability.

- Start with $1,000 as your initial goal

- Expand to 3-6 months of living expenses

- Use high-yield savings for better returns

- Never touch it except for true emergencies

Latest Blog Articles

Expert insights and in-depth guides to help you master personal finance

Top 5 Best Personal Finance Apps for Americans in 2024

Discover the best personal finance apps that help Americans manage money, track expenses, and build wealth. Compare YNAB, Mint, Rocket Money, Vanguard, and Credit Karma.

How to Build an Emergency Fund: Complete Step-by-Step Guide

Learn how to build an emergency fund from scratch. Discover how much you need, strategies to save faster, and why it's critical for financial security.

Understanding Compound Interest: The Secret to Building Wealth

Master compound interest and learn how it can turn modest savings into substantial wealth. Includes real examples, formulas, and strategies to maximize returns.

Ready to Transform Your Financial Future?

Start implementing these personal finance tips today and watch your financial situation improve. Remember, the best time to start was yesterday, but the second-best time is today. Take control of your money and build the secure, prosperous future you deserve.

Frequently Asked Questions

Find answers to common questions about personal finance

How much should I save in an emergency fund?

Financial experts recommend saving 3-6 months of living expenses in an emergency fund. Start with $500-$1,000 and gradually increase it. The goal is to have enough to cover unexpected expenses like medical bills, car repairs, or job loss without relying on credit cards or loans.

What's the difference between a 401(k) and an IRA?

Employer-sponsored retirement plans vary by country. In the US, 401(k) and IRA accounts are popular. In other countries, you may have pension schemes, superannuation (Australia), or other retirement vehicles. Check your country's retirement savings options and maximize contributions for tax benefits.

How does compound interest work?

Compound interest is when you earn interest on your interest. For example, if you invest $1,000 at 7% annual return, after year 1 you have $1,070. In year 2, you earn 7% on $1,070, not just the original $1,000. Over time, this exponential growth significantly increases your wealth. Starting early is crucial because time is your biggest advantage.

What are the most common financial mistakes?

Common mistakes include: not having an emergency fund, carrying high credit card debt, not starting to invest early, lifestyle inflation (spending increases with income), ignoring credit scores, and inadequate insurance. Awareness of these mistakes is the first step to avoiding them and building better financial habits.

How can I save for vacation without ruining my budget?

Set a realistic vacation budget, automate savings into a dedicated account, find money in your current budget (reduce dining out, cancel unused subscriptions), earn extra income through side gigs, and plan your trip strategically (travel off-season, book in advance). Never put vacation on credit cards - save first, then travel.

What's the best personal finance app for beginners?

For beginners, YNAB (You Need A Budget) is excellent for budgeting, Mint for expense tracking, Rocket Money for bill management, and Vanguard for investing. Choose based on your needs: if you want budgeting help, try YNAB; if you want expense tracking, try Mint; if you want investing, try Vanguard. Most people benefit from using 2-3 apps together.